REPORT 3Q-2024 | Economic and RE data

- Darian RE

- Oct 21, 2024

- 3 min read

Updated: Sep 23, 2025

General Overview

The strength demonstrated by financial markets during the third quarter of the year—and continuing as of the date of this report—seems to contrast sharply with the international context. The tensions between Palestinians and Israelis have escalated into a full-scale war involving Lebanon and Iran, with the latter launching rockets toward Israel. The approach of the U.S. elections, which saw a shift in the Democratic camp between July and August from the incumbent President to the newly nominated candidate Kamala Harris, adds another layer of uncertainty. However, this development appears to have restored balance between the two parties after President Biden showed significant signs of weakness.

Never before in an election year have U.S. financial markets shown such strength.

Nevertheless, as these trends appear anomalous given the ongoing geopolitical landscape, it is crucial to remain highly vigilant—after all, not everything that glitters is gold. China's economy, for instance, seems to be experiencing deflation, and the slowdown in consumption within one of the largest and fastest-growing economies of recent decades is undoubtedly a cause for concern.

Some Figures

The ECB has kept its promises regarding interest rate cuts, implementing an additional 50 bps reduction, bringing the refi rate to 3.65%. The Fed, too, could no longer postpone action and, in September, cut rates by 50 bps, bringing the benchmark rate to 5%. Similarly, the Bank of England reached the same 5% level after a 25 bps cut in July. These developments suggest that inflation concerns have been contained, allowing renewed discussions on economic policies to support consumption.

Indeed, Germany could end 2024 in a recession. If the government fails to implement the necessary growth measures in time, forecasts predict another contraction of 0.2% in the German economy, following the 0.3% decline in 2023.

For 2024, the Eurozone economy should grow by 0.7%, with Italy forecast at 0.8%, the U.S. at 2.5% (in line with 2023), and the UK at 1.1%, marking a significant improvement over the previous 12 months (OECD economic outlook data).

The Real Estate Market

Italy's real estate market, which was stagnant at the end of the year's first half (based on the latest data from the Agenzia delle Entrate), shows a slight increase in residential property transactions when comparing 2Q 2023 to 2Q 2024. However, when extending the analysis to the entire first half of the year—partially impacted by a sluggish 1Q—a contraction remains. The trend for the metropolitan city of Milan seems to be different; in the economic capital of Italy, residential transactions have slightly declined, even when compared to the same quarters of both years.

According to the FIAIP report, residential property prices in provincial capitals increased by 2.5% between the first half of 2023 and the same period in 2024. The number of property transactions involving mortgages also rose, partly due to the initial interest rate cuts mentioned earlier. Nonetheless, as already observed in 1Q 2024, this quarter also confirms an inevitable slowdown in the market.

Focusing on commercial properties of interest to Darian RE (offices, retail spaces, banks, hotels, and industrial properties), the number of transactions increased at national and regional levels between 2Q 2023 and 2Q 2024. However, Milan and its metro area recorded a contraction. Extending the analysis to previous years, the trends observed are similar.

When comparing the first halves of the year, commercial property transactions in 2024 showed a nearly uniform increase across key geographical areas, supported by a strong first quarter in the Milan market.

As with the first quarter, the year's second quarter also stands out as the best 2Q since 2011.

Contrary to many expectations, the commercial real estate market appears to be in good health. Excluding banks and hotels—where transaction volumes remain too limited to establish a clear trend—office sales (cadastral code A10) grew by 6.5% nationwide (+10.8% in Milan), retail property sales (cad. code C1) increased by 5.5% (+4.9% in Milan), and industrial property transactions (warehouses and industrial buildings) surged by 12.6%, with Milan recording a +9.9% rise.

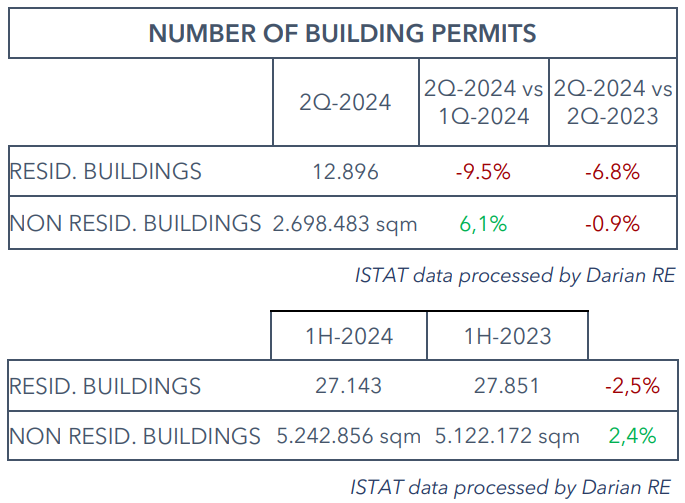

Meanwhile, the number of residential building permits saw a sharp decline, both quarter-over-quarter (2Q 2024 vs. 1Q 2024) and year-over-year (2Q 2024 vs. 2Q 2023). The legislative changes regarding the tax incentives for renovations may be one cause of this decline.

The total square footage of commercial properties approved for construction increased in consecutive quarter comparisons, while a slight decline was recorded in the year-over-year comparison.

Data Sources: Agenzia delle Entrate, ISTAT, and tradingeconomics.com

Data Processing: Darian RE

"We are experts in different real estate markets and property and asset management. Contact us to help you manage your real estate portfolio or for consultancy."

Comments