REPORT 1Q-2026 | Economic and RE data

- Darian RE

- Apr 27

- 3 min read

Updated: May 4

General Situation

If the President of the United States set out to leave a clear mark during his term, he has achieved his goal. In the first quarter of 2026, the 47th (and 45th) occupant of the White House actively asserted American geopolitical and macroeconomic influence.

In early January, the military operation in Venezuela signaled a return to a more proactive US geopolitical stance. Between late February and early March, rising tensions involving the United States, Israel, and Iran escalated into direct military confrontation, with significant implications for the balance of the Middle East.

While some areas are showing early signs of stabilization, the impact is becoming more visible elsewhere.

Iran responded with direct military actions against US Gulf allies. It also carried out indirect disruptions affecting global energy routes, including the Strait of Hormuz. This had a direct impact on oil flows, lifting prices to levels well above $100 per barrel at times.

These developments are expected to drive higher energy prices, renewed inflationary pressure, and a slowdown in global growth.

In this context, pressure on energy supply chains and a contraction in global trade are increasingly likely as direct outcomes.

Europe continues to play a secondary role in the global geopolitical landscape, with internal divisions among member states emerging over policies related to military intervention.

In Italy, rising fuel and energy prices were immediately reflected in consumer sentiment, bringing energy dependence back into focus. GDP growth forecasts for 2026 have been revised downward to 0.5% (sources: ISTAT, European Commission). This figure is even more significant, given that the quarter benefited from the positive impact of the Milan-Cortina Winter Olympics, which boosted tourism and the services sector. At the same time, domestic demand remains weak, and political stability has become more uncertain following the March constitutional referendum, which rejected judicial reform.

Some Figures

The current geopolitical environment leaves limited room for optimism. Oil and gas prices remain highly volatile. This instability does not support markets or forward-looking expectations, which need greater stability. As a result, making precise forecasts remains challenging.

All major global economies are affected. Central banks remain highly cautious. Europe faces a sharper energy shock and, with already low interest rates, has less room to respond, making it potentially more vulnerable than the United States.

Growth in the Eurozone is expected to remain weak, around 0.9% in 2026. This represents an additional risk, especially if combined with a renewed increase in inflation driven by higher energy costs.

Inflation currently remains broadly in line with 2025 levels: just above 2% in Italy, around 2.6% in the Eurozone, and 3.2% in the United States (sources: ISTAT, Eurostat, Bureau of Labor Statistics).

Real Estate Market

The first quarter of the year provides full-year data from the previous year, enabling a more accurate assessment of real estate market trends.

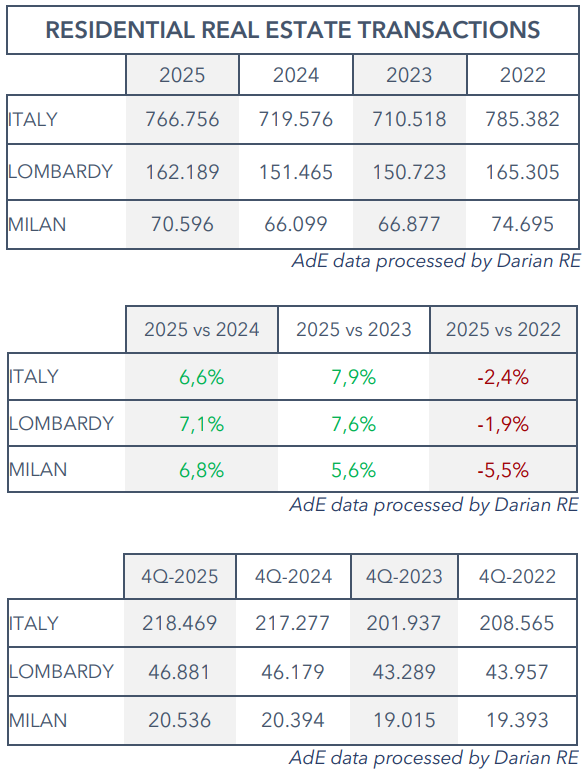

As of 31 December 2025, the Italian real estate market shows solid performance across both residential and commercial segments. The commercial segment includes the asset classes of interest to Darian RE (offices, retail, shopping centers, hotels, industrial assets, and warehouses).

Residential transactions totaled 766,756, second only to 2022 and up 6.6% from 2024. The 4Q-2025 figure was 0.5% above 4Q-2024. Regional transactions rose 7.1%, and in Milan’s metro area, 6.8% (source: Osservatorio del Mercato Immobiliare OMI AdE).

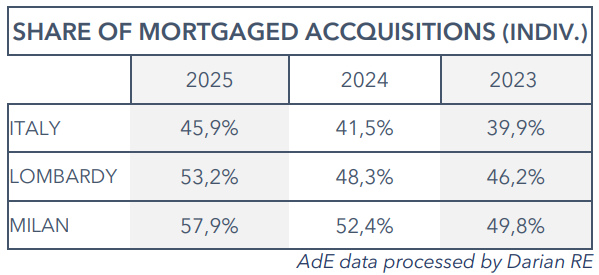

Mortgage-backed transactions increased across all analyzed areas. Since 2023, mortgage-backed transactions have risen by 6% nationwide, 7% in Lombardy, and 8.1% in the Milan metropolitan area (source: OMI AdE).

Transactions for new build units accounted for 6.4% of the total (49,094), a sharp decline from 2024, when they represented 8.63% (62,076 transactions) (source: OMI AdE).

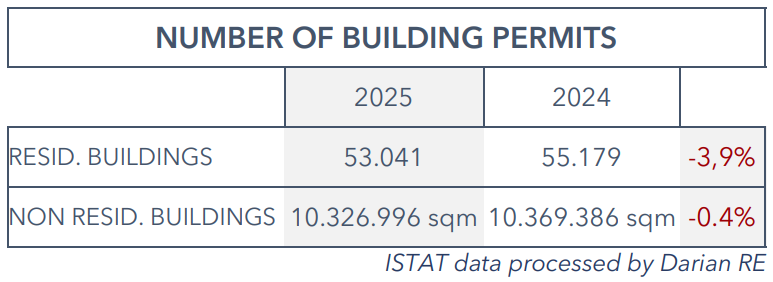

Although not directly aligned due to construction timelines, residential building permits fell by 3.87% in 2025 compared to the previous year. Non-residential permits also drop -0.4% (source: ISTAT).

ISTAT's House Price Index (IPAB) rose 4.1% across Italy in 2025 (provisional data), driven by a 5.2% increase for existing homes that outweighed a 1.2% decline for new housing.

According to immobiliare.it, sale prices in 1Q-2026 increased by 4.3% nationwide, 7.62% in Lombardy, and 5.7% in the Milan metropolitan area. Rental growth was more moderate, at +3.61%, +0.27%, and +1.22% respectively in Italy, Lombardy, and Milan.

Commercial real estate transactions rose, marking the best performance since at least 2011. Nationwide growth was 6.1%, Lombardy saw 3%, and Milan’s metro area stayed mostly stable (-3 units). 4Q-2025 was the strongest quarter since 2011 (source: OMI AdE).

Transaction growth was broad-based across most asset classes. Retail/workshop properties and shopping centers grew 8% nationwide and 7.2% in Lombardy, but declined 1.4% in Milan province. Nationally, office (+3.3%) and industrial/warehouse (+1.2%) transactions also rose (source: OMI AdE).

Data Sources: Agenzia delle Entrate, ISTAT, Eurostat, Bureau of Labor Statistics, and tradingeconomics.com.

Data Processing: Darian RE

"We are experts in different real estate markets and property and asset management. Contact us to help you manage your real estate portfolio or for consultancy."

Comments